No. 56, March 2014

| |

|

|

No. 56, March 2014 |

|

|

No. 56 RBI Under Rajan: Answerable to whom? Royalties: Royal treatment of foreign investors New Bank Licences: For financial inclusion, or exclusion?

|

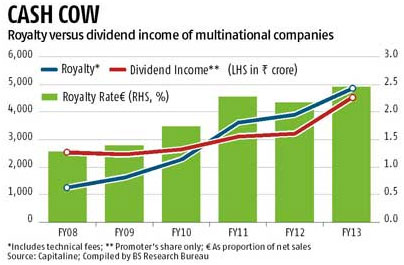

Royalties — by Rahul Varman, rahulv[at]iitk.ac.in The royalties paid by Indian subsidiaries to their foreign parents have been attracting some attention periodically in recent times, but only in the business press. Perhaps this attention is due to the fact that the royalty outflows have been rapidly rising in the midst of an industrial slump. According to Government data, royalty payments have risen from 13 per cent of FDI flows in 2009-10 to 18 per cent in 2012-13. The outflows on account of royalty and fees for technical services, taken together, accounted for 16-33 per cent of the foreign direct investment (FDI) inflows between 2009-10 and 2012-131. A senior Department of Industrial Policy and Promotion (DIPP) official was quoted recently in Economic Times2 as complaining:

Royalty is most often associated with the fee paid to someone who owns a patent for its use or the money owed to an author for each copy of a book sold. It is the share of a product or a profit reserved by the owner for permitting another to use his/her property3. The business press often claims that two key things foreign companies have to offer to India, for which we need to make policies to win their favour and investments, are technology and branding. Foreign firms also generally claim that they are charging high royalties for bringing technology and international brands to their Indian subsidiaries; hence for the purpose of this discussion, royalty is a fee for bringing knowhow and trademarks from foreign shores.

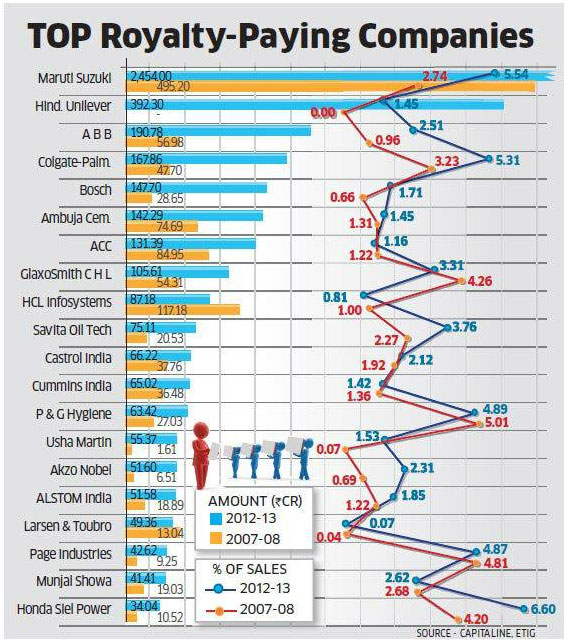

The list of companies here includes all the star MNCs and leaders of their respective industries in the country and globally (see Figure 2 below). Maruti Suzuki has by far the largest royalty bill in India, followed by Hindustan Unilever Ltd (HUL). Maruti’s royalty payment to its Japanese parent Suzuki has risen to Rs 2,454 crore in 2012-13 from Rs 495 crore in 2007-08. At 5.5 per cent of sales, Maruti also tops the chart in royalty rate, followed by Colgate-Palmolive. In 2012-13, companies such as ABB and Maruti Suzuki paid equivalent of over 300 per cent and 100 per cent of their profits after tax (PAT) as royalty and related payments. Companies such as 3M India, Timken India, Whirlpool India and Asahi India Glass have paid royalty in the range of 1.2 per cent to 2.6 per cent of net sales to their foreign partners but have not paid any dividends to shareholders since 2008 (excluding one-off dividend payments). Asahi India Glass paid Rs 20.5 crore as royalty payments though it incurred a loss of Rs 58.7 crore in 2011-126. HUL, India’s largest consumer goods maker, last year agreed to more than double its royalty payout to Unilever from the current 1.4 per cent to 3.15 per cent of sales by 2018 in a phased manner. Around the same time, McDonald’s Corporation, the US-based fast-food multinational company, signed an agreement with its Indian franchisee Hardcastle Restaurants Private Limited (HRPL) for royalty fee of 8 per cent of net sales by 2020, against the current 3 per cent. This would be one of the highest royalties paid by an Indian company to its parent abroad7. Nestle proposed to increase such costs from 3.5% to 4.5% of sales over a five year period, starting 20148.

The timing of royalty payments and ‘convenient’ regulatory relaxations

Source: IIAS Report, 20129 In May 2010 the Government and the Reserve Bank of India (RBI) amended the Foreign Exchange Management Rules, 2000, doing away with the need for the Commerce Ministry to approve royalty payments exceeding 5 per cent of domestic sales and 8 per cent of export sales. Thus all regulatory requirements capping royalty payments to foreign collaborators were done away with in the quest for foreign investments, and the stage was set for massive hike in royalties to the MNCs by their respective subsidiaries. Once this policy began hurting the economy and our foreign exchange position, the Government did make some feeble attempts to stem the flow. For instance, in the last Budget, the Government did raise the tax rate on royalty and fee for technical services paid to overseas entities from the earlier 10 per cent to 25 per cent. Immediately, there were strong reactions from industry lobbies against the hike in tax rates. But in reality this hike is of little consequence as India has signed double tax avoidance treaties with most of the countries in which the parent companies are located, making the effective tax rate only 10-15 per cent. For instance, in case of Mauritius, which is the source of half of FDI flows to the country, such tax rate is only 10 per cent, as per the bilateral tax treaty. The issues raised by high royalty payments

What are the services for which such high fees are being charged?

Take for example the case of Maruti, which is by far the highest royalty payer. In the same years when royalties are spiralling upwards, it is losing market share. Earnings per share have come down from Rs 85 in 2010 to Rs 77 in 2013. These are the same years when royalty payments have rapidly risen by more than 50 per cent. Further, if Suzuki has a majority stake, why should it be charging such high royalty, as it anyway has the right to profits through dividends? Moreover, if all Maruti has been doing at its plants is assembly, as most parts are outsourced, with a significant import component from Suzuki, then why should royalty be calculated as a percentage of total sales? This becomes even more glaring in the light of the statement in 2005 of the MUL Managing Director Jagdish Khattar11: “The Swift is also an example of the growing recognition of Indian intellectual and engineering capability; 25 Indian engineers from Maruti have worked with their Japanese counterparts in Suzuki Motor Corporation for two years to design this world car and prepare it for Indian conditions.” If Maruti’s engineers have contributed to the firm’s recent models, why is it paying the parent such high royalties? One might further ask, if so much indigenous expertise is available, then why shouldn’t Maruti be investing more in research and development (R&D), and building up its capabilities? Instead, in 2009, when Maruti was giving a relatively lower royalty of 3 per cent to the parent firm, it was spending merely 0.4 per cent of sales on R&D. By contrast, Tata Motors was spending 1.2 per cent of sales on R&D12. The case for high royalties by consumer goods leader Hindustan Unilever Ltd (HUL) is even more flimsy. After all, what is the technology required to produce soaps, and why should the company charge royalties for brands that have been around for ages and which have been cultivated through the Indian consumers’ pockets over long years? Again, no justification has been provided by the board of directors for their claim that “3.15 per cent of the net sales” is an “arms length price” (i.e., a fair market price, as between two unrelated parties) for the calculation of appropriate royalty rates, or which of the methods prescribed for valuation of transfer pricing were used. It needs to be added that in 2010, the sum HUL spent on R & D was only 1/5th of its royalty payment to its parent Unilever13. What do high royalty payments tell us about the state of corporate governance in the country? In fact, precisely to take care of such conflict of interests, the new Companies Act passed last year by the Parliament attempts to legislate about what are called Related Party Transactions (RPT), the category in which such royalty payments should fall. In case of an RPT, the new Act mandates that a special resolution should be passed, but only by those members who are not a ‘related party’, thus promising an independent voice to minority shareholders in such cases. Perhaps this explains the haste of companies like HUL and McDonald’s to pass resolutions for steep hikes in the royalty rates as a share of net sales over the next several years, before the Act comes into force. Thus the recent hyperactivity is very much in order to evade the law, though MNCs keep trumpeting how law abiding they are! As an indication of how problematic these policies are, even the proxy advisory firms, which are very much part of the corporate system, have been speaking against them. For instance last year, all the three proxy advisory firms in India that advise institutions and investors in the country, had asked shareholders of ACC and Ambuja Cements to vote against the resolution seeking approval to pay technology and knowledge fee of 1 per cent of sales to the Swiss parent Holcim (with freedom to revise this figure at a later date without seeking fresh shareholder approval)15. In fact the company wanted to make this payout 2 per cent of sales; it was only due to resistance from the independent directors on the board that they decided to scale it down to 1 per cent 16. Where do high royalty payments leave the minority shareholders? However, the issue of royalty payments made to MNC parent firms is not merely one between the parent company and the minority shareholders. It represents a broader question of public interest. Royalty is one of the forms of extortionate extraction by MNCs from Third World countries, resulting in the outflow of foreign exchange and reduction of tax revenues. In the words of the DIPP official quoted at the start of this article, it is a “drain on the economy”. It was on this logic that, in the past, the Indian authorities placed limits on royalty rates. By contrast, today the larger question of public interest is not even mentioned. The DIPP official’s remark was an isolated one, not echoed by senior policymakers, who are too busy trying to woo foreign investment on any terms. Interestingly, it is now mainly private investors in these firms (including foreign institutional investors) who are raising the issue of exorbitant royalty payments from the narrow angle of their financial interests. In conclusion Against this background, let us look at the treatment meted out by the MNC subsidiaries to another part of the same company, that is, the workers. We need go no further than our largest royalty payer, Maruti. In the very period in which Maruti’s royalty payments have been skyrocketing, the workers of its Manesar plant have been agitating for their constitutional right of association, the right to form a union of their own choice, and for their dignity, such as proper rest breaks. The 2000-odd workers have kept agitating heroically in the face of harsh repression by the management and the State. Finally this long agitation culminated in the tragic violence of 2012 and death of a Maruti manager, and since then the systemic hounding of workers and their leaders. 147 workers have been in jail for almost two years on very serious charges, despite the lack of any evidence against them. What would it have cost the company if the wages of all the 2000 workers were increased by say a ‘princely sum’ of Rs 10,000 per month? All of Rs 24 crores annually! This is .05 per cent of the total income of the company and mere 2.5 per cent of the total wage and salary bill of Maruti last year18. Contrast this with the royalty bill of close to 2,500 crores last year. In an extension of the same trend, last month Maruti Suzuki announced that its proposed new factory in Gujarat will be owned not by it (as was originally planned) but by a fully-owned subsidiary of the parent, Suzuki Motor Corporation. Under the new arrangement, the new factory will produce cars which will be sold by Maruti Suzuki. Maruti clarified that the new company will sell the cars at ‘cost price’ and not at a profit. The management claims that the price will be determined on an “arm’s length” basis and the components will be sourced by Maruti Suzuki. So, it was said, there is no way profits would get transferred from the widely-owned Maruti Suzuki to closely-held Suzuki Motor Gujarat. But the difficulty is that, as in the case of royalties, the whole deal is going to be opaque and the real returns are likely to be made through the transfer pricing on services and inputs bought from the parent in Japan. The wholly-owned subsidiary will not be required to provide information regarding its costs, as would Maruti. A further factor behind this decision could be the wish to insulate the Gujarat Suzuki workers from the struggles in Maruti units, and to tighten control over the workers. A former executive of Maruti Suzuki is quoted as saying, “Foisting the Japanese method of labour management on Manesar has been a disaster. So it is quite tenable that Suzuki wanted Gujarat to have nothing to do with the existing unions and it prefers to deal with the unions directly rather than through the Indian company.”19 Let us take another example, that of global cement major Holcim, and its two Indian subsidiaries, Ambuja and ACC. Last year Ambuja and ACC together paid close to Rs 300 crore royalty to Holcim (see Figure 2). The 1000-odd contract workers at ACC Holcim’s Jamul plant in Chhattisgarh have been struggling since 2011 for regularisation. Some of them have been working in the company for decades and have even won their case in the High Court. Yet they have not been granted their legal rights. They work on a pittance of Rs. 150-200 a day without any rights and dignity while the CEO has an annual pay packet of Rs 10.5 crore20. Similarly, in another plant of Holcim, this time belonging to the subsidiary Ambuja in the same state, where the contract workers have been trying to organise, the young leaders have been falsely implicated for ‘looting’ Rs 3500 and mobiles and put behind bars! In 2010, before attempts at organising began, the contract workers in this plant were not even being paid minimum wages. In addition to the workers’ share, the company was deducting even its own share of the Provident Fund contribution from the extremely paltry wages of these contract workers which is absolutely against the law. The company even deducted charges for helmets and boots21! In the days of the Permanent Settlement more than 200 years ago, the East India Company decided to charge fixed lagan (land rent) from the peasants of the Bengalsuba. This had devastating consequences for the peasantry as, even during the bad and drought years, they were forced to pay rents at the same fixed rate. The company and the intermediaries made massive returns at the cost of sweat, blood and toil of the peasantry. Looks like little has changed in the intervening two centuries: while the producers toil without any rights, dignity or returns, our foreign masters have assured and ever increasing extractions.

Notes: 1. http://profit.ndtv.com/news/industries/article-finance-ministry-examining-dipps-proposal-for-curbs-on-royalty-payments-377559. Please note that this does not include other kind of outflows like dividend payments and payments for components/ parts and machinery imported from foreign shores. So it will be an interesting question to examine what the net investment flows are to the economy through these companies. (back) 2. http://articles.economictimes.indiatimes.com/2013-12-23/news/45510124_1_royalty-payments-abb-india-nestle-india (back) 3. The term royalty is also used for the payment made by firms to governmental authorities for the mining of minerals. (back) 4. http://www.business-standard.com/article/companies/royalty-bigger-than-dividends-for-mncs-114011701117_1.html (back) 5. The ratio of operating income (earnings before interests and taxes) to net sales. (back) 6. http://www.business-standard.com/article/companies/investors-want-more-say-in-royalty-payment-113100201016_1.html (back) 7. http://www.business-standard.com/article/companies/mcdonald-39s-seeks-higher-royalty-from-india-arm-113010900130_1.html (back) 8. http://articles.economictimes.indiatimes.com/2013-12-23/news/45510124_1_royalty-payments-abb-india-nestle-india (back) 9.Institutional Investor Advisory Services, “Royalty payments and minority shareholders”, December 11, 2012, http://www.iias.in/downloads/institutional/Royalty%20payments%20and%20minority%20shareholders%20%28Final%29.pdf (back) 10. Ibid. (back) 11. Quoted in http://archive.tehelka.com/story_main14.asp?filename=Bu111905Maruti_wants.asp# (back) 12. inGovern Governance Services, “Royalty Payments to Group Companies”, August 2010, http://www.ingovern.com/wp-content/uploads/2011/03/Corporate-Governance-Debate-August-2010.pdf (back) 13. Ibid. (back) 14. See for instance the report on the Unilever hike in royalty by the corporate governance advisory firm Stakeholder Empowerment Services: http://www.sesgovernance.com/admin/images_store/HUL_Royalty%20Payment%20Final.pdf (back) 15. http://www.mydigitalfc.com/companies/investors-oppose-acc-ambuja-tech-fee-559 (back) 16. http://www.business-standard.com/article/companies/mcdonald-39s-seeks-higher-royalty-from-india-arm-113010900130_1.html (back) 17. 52/efficiency.html (back) 18. http://www.capitaline.com (back) 19. http://www.business-standard.com/article/companies/what-suzuki-s-gujarat-plant-means-for-maruti-114013001476_1.html (back) 20. Update dated April 20, 2011 from Friends of Chhattisgarh Mukti Morcha (back) 21. Update dated January 15, 2014 from Pragatisheel Cement Shramik Sangh (back)

|

||||||||||||||||

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|||||||||||||||||

|

All material © copyright 2015 by Research Unit for Political Economy |

|||||||||||||||||