No. 56, March 2014

| |

|

|

No. 56, March 2014 |

|

|

No. 56 RBI Under Rajan: Answerable to whom? Royalties: Royal treatment of foreign investors New Bank Licences: For financial inclusion, or exclusion?

|

RBI Under Rajan Answerable to Whom? Nowadays the Reserve Bank of India (RBI) is often in the news. However, people are largely in the dark about what it does, and why. True, the press tell us that when the RBI hikes the ‘repo’ rate (the interest rate at which the RBI makes short-term loans to commercial banks), the cost of home and automobile loans is expected to go up, since the banks’ cost of funds rises; and, correspondingly, the reverse is expected when the RBI reduces the rate. Yet we need to understand more about the RBI’s policies, since they have an impact on the lives of the common working people, not merely on the buyers of flats and cars. Indeed, the RBI’s policies seem set to have an even bigger impact in future, as international financial capital tightens its grip on our country’s economic decision-making process itself. The recent appointment of Raghuram Rajan as governor, and the policies he has initiated in his first four months of office, have far-reaching implications. Let us look at some recent developments in order to get an idea of what the RBI is up to, and where it is heading. In the name of inflation control Why should it matter to us what international financial capital thinks? The reason is that the Indian economy runs up large external deficits.1 It does so not because that is the inevitable fate of underdeveloped economies, but because the rulers implement policies which create such deficits. To take just one striking example: the liberalisation of gold imports led to a massive increase in this already large and economically useless head of import. The Indian propertied classes, dissatisfied in recent years with the low returns in the depressed stock market, turned to buying gold biscuits on a large scale. So large was the gold import boom that, of the merchandise trade deficit (excluding oil) of $87.2 billion in 2012-13, gold alone accounted for $47.2 billion. In other words, the country added an additional $47 billion to its foreign liabilities that year just to pay for the gold imports of the propertied class. Gold, of course, is far from being the only unjustifiable import, but it epitomises the manner in which scarce foreign exchange is squandered. Thus it is State policy that creates large current account deficits; and since the economy requires continuous, large inflows of foreign capital to bridge these deficits, the country’s rulers are in no position to ignore the demands of foreign investors. It was precisely in order to gratify international finance that, as dollars were flying out of India and the rupee’s value plummeted, the Government appointed Raghuram Rajan as Governor of the RBI. Religious beliefs Instead of boosting demand, these economists say, the Government should focus on improving the ‘incentives for savings’ (translation: improving returns to private capital, since it is only the wealthy who can save substantial sums). They spell out the steps to boost savings as follows: (i) make labour ‘competitive’ – i.e., give employers greater freedom to fire workers and to reduce wages, curtail assistance to the unemployed, and thus force the unemployed to accept work at any wage;2 (ii) relax laws/regulations which constrain or displease large private investors (i.e., relax or do away with environmental laws, labour laws, aid/protection to small firms, checks on monopoly control, restraints on foreign investment); (iii) wind up Government presence in various sectors in order to leave those sectors free for private investors; and generally take all measures needed to please private capital and thus revive business ‘confidence’. A return of ‘confidence’ will lead private investors to invest, and that alone can revive the economy. According to the head priest of this sect, such steps would literally be a hundred times as effective as Government spending to boost demand and prevent a recession/depression.3 It is not hard to see why, despite the obvious flaws in this model and the ruinous record of its practice, big capitalists, particularly in high finance, like the sound of a theory that says that the aim of State policy must be to keep them happy. However, unlike the academic economists who invent and propagate such theories, and must cling to them even in the face of contrary evidence, capitalists can promote, modify or dump such theories according to their current requirements. In fact, the global crisis that broke in 2008 compelled policy-makers to partially (and temporarily) revise the view dominant in academic economics. The policy-makers revised their position not because the crisis discredited the myth that markets were always rational and efficient (which it did); nor because the crisis created large-scale, persisting unemployment and suffering (which it did); but simply because big business needed bailing out and stimulus to grow. Thus, despite the erstwhile dominance of the markets-are-infallible-and-adequate school in the US, when the US ruling classes’ own vital interests were affected, the US government sidelined it temporarily. The US incurred massive fiscal deficits in order to bail out its financial sector and to a much lesser extent its automobile industry. The US central bank, the Federal Reserve, not only reduced interest rates to rock-bottom levels, but pumped gigantic sums of money into the economy by buying up financial instruments. Thus the US economy is now growing faster than many of the poorer economies that were earlier said to be rapidly catching up with the advanced countries. It is worth noting that the central bank of the US explicitly states that its objectives include not only stable prices, but growth and employment. Other central banks, such as the European Central Bank (ECB) and the Japanese central bank, similarly dumped the theory that all intervention would be useless/harmful, and instead pursued interventionist policies to boost demand.4,5 By contrast, here is Raghuram Rajan’s first statement on becoming governor of the RBI (September 4, 2013):

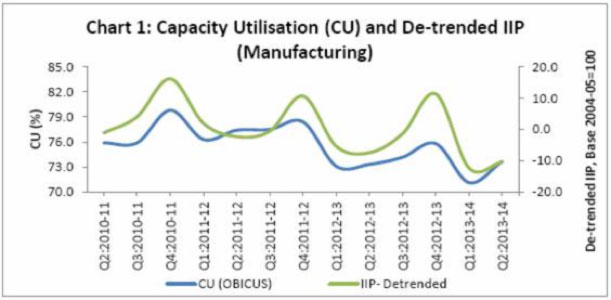

In other words, whether or not the nature of the inflation is such that it can be controlled by the central bank, the central bank must assume it does and give primacy to checking inflation with monetary measures. It seems that what international finance wants Third World countries like India to do is not to follow the demand-boosting easy-money policies followed during 2008-14 in international finance’s own citadel, but to stick to a one-point policy of demand-suppression – and this, in economies which already have low average levels of consumption. Monetary Policy Framework Committee The report begins by admitting that “Drawing from the lessons of the global financial crisis, there is a consensus gathering internationally that monetary policy should move away from its narrow focus on inflation.” It then proceeds to ignore that consensus: “Yet, given the initial conditions facing India at the current juncture, bringing down inflation must be accorded primacy.”6 (emphasis added) What are those “initial conditions” facing India at the “current juncture”? No doubt, inflation is high, particularly in food and fuel. At the same time, there is an economy-wide recession due to paucity of demand. For the last three years, industrial growth has been slowing down sharply, and has now turned negative – i.e., industrial production is shrinking. Capacity utilisation in industry has shown a downward trend for three years. Given that even existing capacity is being under-utilised, it is hardly surprising that the production of capital goods (goods which increase future productive capacity) has actually fallen for the past two years. The share of GDP going to fixed productive assets has declined steadily for six years. Consumption expenditure growth too has been slowing for the past three years, and is now at a near-standstill. Even growth in the services sector, the biggest component of India’s economy, has been slowing down steeply for three years, and is at its lowest level in 12 years. What this tells us is that high inflation can co-exist with low demand, if the factors leading to inflation are ‘cost-push’, not ‘demand-pull’. If a war in West Asia leads to a rise in the price of oil, this price rise cannot be laid at the door of excess demand, and even if the incomes of all Indians were halved the price of imported oil would not go down. But in noting the “initial conditions” at the “current juncture”, the committee blithely disregards the recession, and focuses only on the inflation. It prescribes ‘inflation targeting (IT)’, whereby the RBI announces a particular target for the inflation rate, and attempts to achieve it using interest rates. The intellectual pedigree of inflation targeting In fact, the IMF has been pressing India for over a decade to adopt inflation targeting. However, the RBI has been reluctant to do so; the last governor even explicitly ruled it out as being inappropriate in the Indian context. Whereupon an ex-employee of the IMF has been parachuted in as RBI governor, and has promptly adopted inflation targeting. Non-monetary factors driving prices The reader may well wonder what the difference is between a “persistent” short-run factor and an actual medium-run factor. In fact, over the last six years, the contribution of food to wholesale price inflation has averaged over two-fifths (see chart below), and it currently accounts for almost half. This despite the fact that food makes up less than a quarter of the wholesale price index. (Its share of the basket of the Consumer Price Indexes is much higher, at least double that in the Wholesale Price Index.) Rise in the prices of fuel and minerals is directly responsible for almost a quarter of the rise in wholesale inflation (see chart). So, putting food and fuel together, at least two-thirds of current wholesale inflation comes from sources which the report itself mentions are “not easily controlled by monetary policy” (in 2013-14 three-fourths comes from these sources). And since food and fuel prices also feed into the prices of all non-food manufactured goods (in the form of higher wages and input costs), the real influence on overall prices of these items “not easily controlled by monetary policy” is even higher. They have persisted, even grown, over the last few years. If the Government would indeed tackle these sources of so-called “short-run” inflation, people may not be too worried about the RBI’s theories about “medium-run” inflation being monetary. People live their whole lives in the “short-run”, and their “medium-” and “long-run” are merely aggregates of their “short-run”.

Second disadvantage – IT may reduce employment, not prices Such was the case, for example, when interest rates were hiked 13 times between March 2010 and October 2011, at the end of which annual consumer inflation (for industrial workers) was still as high as 9.4 per cent and annual growth of the Index of Industrial Production was -5.1 per cent, i.e., industrial production was falling. In the words of the report, “Yet another concern [with inflation targeting] has been the instability imparted to output and employment due to the overarching emphasis on achieving the inflation target, and the observed increase in output losses associated with disinflation.” While the pre-Rajan RBI claimed to pursue a ‘multiple-indicator’ policy, i.e., not solely targeting inflation by suppressing demand, but also keeping in mind growth, in practice it gave demand-suppression greater weight. After the 13 successive rate hikes (raising the repo rate from 4.75 per cent to 8.50 per cent) failed to reduce inflation to reasonable levels, but deepened the industrial slump, the RBI wavered in its determination to beat the economy to death. It lowered rates partially, to 7.25 per cent by May 2013. But this half-hearted reduction failed to make any positive impact on industrial growth. The MPF Committee report takes the results of this lopsided policy, a policy lopsided in favour of inflation targeting, as evidence of the need to go whole hog, and abandon output and employment altogether: “In recent years, however, there has been mounting public censure of the efficacy and even the credibility of this [multiple-indicator] framework as persistently high inflation and weakening growth have come to co-exist.” (p.9) The point is, the very fact that persistently high inflation and weakening growth co-existed should have alerted the Committee to the fact that demand-suppression would not work. They co-existed even during the period of 13 rate hikes, which, given the actual sources of inflation, were a recipe for stagflation.9 The Committee feels that if the RBI takes output and employment into account in deciding its policies, it will be unable to anchor inflationary expectations. “It also leaves policy analysts unclear about what the RBI looks at while taking policy decisions.” (p. 9) The whole point is, according to them, to make the RBI’s intentionsclear to the public at large; that will check inflationary expectations; and that will check inflation itself.10 Perhaps not in the short-run, but in the medium-run; unless the short-run factor is persistent, in which case, not in the medium-run either; but the RBI will have done its duty. The Committee asks: “The crucial question, therefore, is: what is driving household inflation expectations in India?… expectations are significantly influenced by food as well as fuel inflation measured from CPI-IW….” (p. 16) In fact, “Shocks to food inflation and fuel inflation also have a much larger and more persistent impact on inflation expectations than shocks to non-food non-fuel inflation.” In other words, it is when people experience a rise in food or fuel prices that they are most likely to expect prices to keep rising. The ordinary, untrained, reader, like us, might conclude from this: Whatever is causing food and fuel prices to rise should be checked by direct Government action, both medium- and short-term (increasing public sector investment in agriculture to improve supply, storage and distribution; extending the coverage and reach of the agricultural procurement and public distribution system; halting exports of food commodities and checking hoarding/speculation; restraining the diversion of vegetables, milk and sugar to corporate sector processed foods industries; reducing taxes on petroleum products to bring their prices down; checking private sector profiteering in the power generation sector, and halting the rise in electricity tariffs; acting against industrial cartels in sectors such as cement and steel; and so on). That would do both jobs: It would directly reduce prices, and it would bring down inflationary expectations, preventing an upward spiral. More importantly, it would do so in such a way as not to reduce employment, and thus protect the incomes of the majority of people. But no: in the Committee’s view, precisely because monetary policy can’t affect food and fuel prices, it must hammer inflationary expectations down all the more vigorously. “Since food and fuel account for more than 57 per cent of the CPI on which the direct influence of monetary policy is limited, the commitment to the nominal anchor would need to be demonstrated by timely monetary policy response to risks from second round effects and inflation expectations in response to shocks to food and fuel.” (p.20) (Since people in this theory are presumed to be perfectly informed of economic policy and its impact, would they not also know that monetary policy can’t do much about food and fuel prices, and hence ignore it?) Placing monetary policy beyond the reach of public pressure The Committee recommends that the RBI should adopt the new Consumer Price Index (combined) as the measure of inflation for the purpose of triggering interest rate changes. Since the share of food in the CPI is about double of its share in the Wholesale Price Index, the shift to the CPI as the measure means that the RBI will be even more energetically hammering away at suppressing demand. The Committee has set the target inflation rate at 4 per cent, with a band of +/- 2 per cent around it, and it has set a path for achieving it (8 per cent by 2015, 6 per cent by 2016). In order to further secure this policy from any “pressures from interest groups”, the Committee recommends that decisions regarding monetary policy should be taken out of the hands of the RBI governor, since he remains accountable to the Government of India (the RBI Act states that the Central Government shall appoint and remove the Governor and may give the RBI directions in the public interest.) Instead, monetary policy making should be vested in a monetary policy committee (MPC), which will include two members external to the RBI. The RBI will release a bi-annual inflation report, and “the MPC will be accountable for the failure to establish and achieve the target inflation rate. Failure is defined as the inability to achieve the inflation target of 4 per cent (+/- 2 per cent) for three successive quarters. Such failure will require the MPC to issue a public statement, signed by each member, stating the reason(s) for failure, remedial actions proposed and the likely period of time over which inflation will return to the centre of the inflation target zone.” (p. 28) On the face of it, it seems rather pleasing that Government officials are being held accountable, and that too for such a crucial job as bringing down inflation. However, since the MPC cannot be held accountable for “external shocks” like food and fuel price hikes, what the above rule ensures is not the result, i.e., 4 per cent inflation, but the means to be used (change in interest rates) any time inflation is out of the target zone. Moreover, the MPC is required to ignore the state of output and employment; it is answerable for inflation alone. The real point is the exact oppositeof public accountability: it is to install a financial dictatorship in charge of monetary policy. Not only monetary, but even fiscal policy under the financial dictatorship

The implication of the last sentence is: If the Government doesn’t slash spending, the RBI will keep interest rates punishingly high, forcing the Government to fall in line. This amounts to the RBI dictating fiscal policy. On the same page, the report provides a table of countries which have adopted inflation targeting at one point or the other since 1990, and claims to show that they all reduced their fiscal deficits dramatically thereafter. What is the connection, since inflation targeting is done by the central bank, and the fiscal deficit is in the hands of the Government? The connection is implied: that the central bank holds the whip of interest rates, and forces the Government to fall in line and reduce spending. “Fiscal discipline generally turned out to be the biggest immediate advantage of formal adoption of inflation targeting.” (p. 21) As it is, the share market, in which the foreign institutional investors call the shots, places enormous pressure on policy-making. Recall that last year, when the Food Security Bill was passed in Parliament, the rupee and the share market promptly sank, and the corporate media chorused its disapproval of the Bill. The headline of one financial paper ran: “Rupee, Sensex sink on fears Food Bill will feed deficit.”11 With the MPC, this pressure would get an additional institutional arm. Further, the committee says: “Administered setting of prices, wages and interest rates are significant impediments to monetary policy transmission and achievement of the price stability objective, requiring a commitment from the Government towards their elimination.” Nor should the Government interfere by telling banks (even public sector banks, of which after all the Government is still the owner) how much interest to charge: “Government should eschew suasion and directives to banks on interest rates that run counter to monetary policy actions.” (p. 48) For example, the Committee says, the Government should not try to keep interest rates on agricultural credit low: “With a sharp rise in the ratio of agricultural credit to agricultural GDP, the need for subventions on interest rate for lending to certain sectors would need to be re-visited.” (Ibid.) This is also the recommendation of another Rajan-appointed committee, the Nachiket Mor committee,12 which recently submitted its report. Mor and co. recommended doing away with lower rates for agriculture, small-scale industry, and so on. All these sections would be left to the winds of the market. We have already seen what this means, with micro-finance institutions charging upward of 24 per cent interest on their micro-loans, no different from any usurer, and in fact pushing borrowers to commit suicide. Such so-called ‘market-determined’ rates – in an economy which is abysmally un-integrated and socially stratified, in which 90 per cent of small businesses have no links with formal financial institutions and 60 per cent of the population do not even have a functional bank account – wind up bleeding the small producer and fattening parasitic sections. And this is the recommendation of a committee supposedly set up to improve ‘financial inclusion’! Latest repo hike: MPF Committee’s recommendations in action Let us look at the RBI’s own report on “Macroeconomic and Monetary Developments” report released along with the RBI’s rate hike. This document tells us that industrial output is in the doldrums:

This time the services sector too is in a slump:

Bank credit has slowed, and the mounting bad debts of the banks are a growing weight on the system:

The Government’s tax revenues bear out the slowdown:

Lower tax revenues, and depressed GDP, will make it even harder for the Government to meet its target of bringing down the fiscal deficit in 2013-14. What is set to depress the economy further is the Government’s determination to slash spending in order to adhere to its fiscal deficit targets:

This cut in Government consumption expenditure is taking place amid an overall slump in consumption expenditure, as shown by the chart below.

Unsurprisingly, the RBI has difficulty painting a positive picture of the situation: “Prospects of a pick-up in real GDP growth in the second half of 2013-14 have been dampened by negative growth in industrial production over two consecutive months, sluggishness in services sector activity and the weakening in private consumption and investment demand.” The RBI’s survey shows businesses continue to expect contraction. Rajan himself says: “The slowdown in the economy is getting increasingly worrisome. Our current assessment is that growth is likely to lose momentum in the third quarter of 2013-14, with industrial activity in contractionary mode, mainly on account of manufacturing. Lead indicators of services also suggest a subdued outlook, barring some pick-up in transport and communication activity.” All this indicates that current inflation is not the ‘pull’ of domestic demand, but ‘cost-push’. Indeed, price rise is being driven by food and fuel, which account for 78 per cent of the increase in the Wholesale Price Index in April-December 2013. Rice prices rose 20 per cent (among the reasons for which was an “upsurge in exports”!). The report says that, because of “weak demand conditions”, prices of non-food manufactured products grew more slowly; this was despite the fall in the rupee’s exchange rate, and despite the rise in input costs. Revisions in administered prices hiked up fuel inflation even when the price of oil fell internationally. Moreover, as Rajan himself pointed out, the immediate spike in consumer prices in April-November 2013 resulted from vegetable and fruit prices, which were already slowing in December and were set to fall in January-February 2014. The RBI has exactly zero influence on vegetable prices. As Rajan also noted, “agricultural performance has so far been robust, and the strong pick-up in rabi sowing indicates that this should be sustained,” which indicates the rate of rise in food prices may slow down, thanks mainly to weather conditions. The real force behind the MPF Committee report: International capital In anticipation of this, Rajan said in his December 2013 policy statement itself: “There are obvious risks to waiting [before hiking interest rates], including the possibility that tapering of quantitative easing by the US Fed may disrupt external markets and that the Reserve Bank may be perceived to be soft on inflation.” (emphasis added) In his January policy statement, he declared: “given the uncertain external environment, the government and the RBI cannot pause in their efforts to ensure fiscal and monetary stability.” (emphasis added) And so the repo rate was hiked once again. In an interview, he explained that foreign investors “are worried about inflation and hence bringing down inflation is a way of assuaging those investors about the long-term future of the country and their investments.”14 Whether or not inflation would actually be brought down by such actions, it was necessary to show foreign investors that the central bank was there to assuage them. The deputy chairman of the Planning Commission, Montek Ahluwalia, supported Rajan’s action: “internationally, he is right to give the signal that we are going to do whatever is necessary.”15 This is the real force behind the MPF Committee report. Flows of international capital are dictating domestic policy. If the Indian government (or for that matter, Turkish, South African, Brazilian, or any other Third World government) tries to revive demand by lowering interest rates and expanding Government spending, foreign investors will exit, their currencies will crash, and their economies will go into a crisis. In order to exercise any control over the domestic economy it would need to impose controls on foreign capital’s entry and exit, but the nature of class rule in such economies (tied to international capital) prevents such an eventuality. Instead the rulers make the economy even further dependent on foreign capital.16 As pointed out recently by Dani Rodrik and Arvind Subramanian, “Over the last five years in India, every episode of rupee pressure has provoked a relaxation of regulations on foreign inflows, which has rendered the economy vulnerable to the next rupee shock, which, in turn provokes the next liberalisation, and so on.” 17 In a word, the Rajan-led RBI’s call for the independence of monetary policy from the Indian government is merely in order to subordinate that policy even further to fickle flows of international capital. End Note: Why foreign finance presses for a one-point programme of ‘inflation control’ There are several reasons for foreign financial investors’ one-point focus on ‘inflation control’.18 (We put this phrase in quotation marks for a reason, which we will explain later.) First, financial investors’ assets are stated in rupee terms. When inflation takes place, the value of the rupee falls, and the financial investor stands to lose in real terms. There is a further angle to this for foreign investors in underdeveloped countries like India. Foreign investors fear that a fall in the internal value of the rupee would lead to a fall in its external value – i.e., the exchange rate of the rupee (vis-a-vis the dollar and other such currencies). Such a fall in the exchange rate could wipe out their returns. To illustrate this, let us take the example of a foreign investor who has invested $100 in India when the exchange rate was Rs 50/$. He buys, let us say, Rs 5,000 worth of shares. After some time, the price of his shares has risen to Rs 6000. He wants to sell his investments and convert the proceeds back to dollars. However, he finds that meanwhile, the rupee has fallen in value, to Rs 60/$, and he winds up getting back only $100 – a zero per cent return. There is another reason for financial investors’ single-minded obsession with ‘inflation control’. The measures which they press for in the name of inflation control – in particular, raising of interest rates and slashing of Government expenditure – open up various rich avenues for profit-making by private investors. High rates of interest may make domestic firms go bankrupt, and become easy prey for foreign capital (this is precisely what happened when the IMF forced southeast Asian countries to steeply hike their domestic interest rates in 1997-98; a large number of businesses in the region were taken over by US investors). When the Government cuts back on its own investments in different sectors, it opens up these sectors to private takeover – mining, railways, ports, airports, power generation, etc, etc. In many cases this involves the creation of private monopolies, or the transfer of valuable natural resources to private hands. The Government is also forced to raise funds by selling off its firms at distress prices. Finally, in its desperation to revive growth, the Government tries to attract private investors by providing them various open and hidden subsidies, and the financial sector is able to reap a part of the rewards. In all these ways, financial investors stand to actually gain by ‘anti-inflation’ measures. Meanwhile, the common people gain nothing and lose much as a result of these ‘anti-inflation’ measures, even though they are usually instituted in the name of saving the poor from the ravages of inflation. (i) For the people inflation is a menace because it eats into their income. Since these supposedly anti-inflation measures being demanded by foreign finance also reduce overall productive activity and employment, any gains to the people on account of lower inflation are wiped out by the fact that their incomes get depressed. What good is the fact that prices are rising more slowly, if your income is rising even slower, or even falling? (ii) The same foreign interests which put pressure for interest rate hikes and cuts in Government spending also put pressure at the same time for the Government to ‘cut subsidies’ – i.e., to raise the prices of coal, petroleum products, natural gas, electricity, and other such ‘administered’ prices, in order that the private sector can make profits in these sectors. Since these commodities are inputs into all commodities, raising their prices fuels further price rise. And so price rise may not really stop, despite the supposed anti-inflation programme. (iii) What happens then is that working people’s incomes fail to keep up with price rise. As their incomes are squeezed in real terms, that reduces the demand for goods. That may eventually bring about a slowing of price rise, but at the cost of the people. We can see this process in action even now. On the one hand the current recession in industry and in construction activity, as well as the sharp reduction of employment under the National Rural Employment Guarantee Scheme, have reduced productive activity and employment. On the other hand, the continued rise in Government-administered prices of fuel and electricity has contributed to the overall price rise.19 As the combined result of reduction in employment and rise in administered prices, the rate of growth of agricultural wages (in real terms – i.e., after accounting for inflation) has plummeted, and looks set to fall further.

NEXT: Royal Treatment of Foreign Investors

Notes: 1. See Aspects no. 54. (back) 2. Rajan and his ilk accompany this with homilies about educating or retraining ‘uncompetitive’ workers for new jobs – even though the problem is not a paucity of trained workers to fill new vacancies, but a paucity of jobs even for educated, trained workers. (back) 3. http://pages.stern.nyu.edu/~dbackus/Taxes/Lucas%20priorities%20AER%2003.pdf Quote: “(Macroeconomics’) central problem of depression prevention has been solved, for all practical purposes, and has in fact been solved for many decades.” – Robert Lucas, 2003. (back) 4. That does not mean that the rulers of the advanced countries have embraced a full-fledged programme to boost demand and employment; far from it. In particular, Government spending has been restrained and ceilings are being placed on Government debt. Ruinous ‘austerity’ measures (cuts in Government spending) are being forced on countries such as Greece and Spain. Such measures are prolonging the depression. The financial sector of the advanced countries, having been the main beneficiary of the bail-outs, is now raising the alarm against Government spending. The current confusion in the ‘mainstream’ economics profession there is illustrated by the fact that the last ‘Nobel’ prize for economics was jointly awarded to a devout believer in the perfection and rationality of markets, who denies the very possibility of speculative bubbles, and another economist whose work demonstrated markets’ tendency to irrationality and bubbles. (back) 5. And despite the dire warnings of the monetary zealots, inflation has not risen in the US, Europe or Japan; on the contrary, in some countries there is a threat of falling prices. Annual consumer inflation in the advanced countries was just 1.5 per cent in November 2013, and the Japanese central bank actually set a target of raising the inflation rate to 2 per cent by January 2015; the US Federal Reserve too has not yet met its target of raising inflation to 2 per cent. (back) 6. p. 5 (back) 7. Financial Services Authority, U.K., The Turner Review: A regulatory response to the global banking crisis, March 2009, p. 5, http://www.fsa.gov.uk/pubs/other/turner_review.pdf. (back) 8. Ibid.; see pp. 39-49 of the report for a survey of the theoretical issues involved. (back) 9. Stagnation plus inflation: A situation where, at the same time, the inflation rate and unemployment rate are high and output growth is low or negative. (back) 10. “Just the place for a Snark! I have said it twice:/That alone should encourage the crew./Just the place for a Snark! I have said it thrice:/What I tell you three times is true.” – Lewis Carroll, The Hunting of the Snark. (back) 11. See Harish Khare, “This perverse rage against the poor”, Hindu, 30/8/13. (back) 12. RBI, Committee on Comprehensive Financial Services for Small Businesses and Low-Income Households, January 2014. (back) 13. New York Times, 30/1/14. (back) 14. Mint, 29/1/14. (back) 15. Business Standard, 29/1/14. (back) 16. The recent stabilisation of the rupee’s value, for which Rajan has won much praise, was partly due to the addition of another $34 billion of high-cost foreign debt to the existing debt stock. (back) 17. “Emerging markets’ victimhood narrative”, Bloomberg, 2/1/14. (back) 18. We have covered this question in earlier issues of Aspects, and apologise for the repetition. (back) 19. The Government’s policies with respect to agriculture and food have played the biggest role in fueling price rise, but administered prices too have accounted for a sizeable share. (back)

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2015 by Research Unit for Political Economy |

|