Nos. 72 & 73, May 2018

| |

|

Nos. 72 & 73, May 2018 |

|

|

Nos. 72 & 73 (May 2018) India's Working Class Under Neoliberal Rule -- RUPE Labour in Global Value Chains: Leather & Footwear Cluster in Kanpur -- Manali Chakrabarti, Rahul Varman Kanpur Leather Cluster Revisited after a Decade -- Manali Chakrabarti, Rahul Varman Simmering Rage I: Discontent and Militancy among Garment Manufacturing Workers in Gurgaon -- Archana Agarwal Simmering Rage II: Bengaluru’s Garment Workers: A Note -- RUPE Fragmentation in the Industrial Working Class and the Crisis of the Trade Union Movement -- Alok Laddha and T Venkat Some Experiences of Organising Workers in Chhattisgarh -- Sudha Bharadwaj

|

India's Working Class and its Prospects Labour in Global Value Chains:

A Study of the Leather and Footwear Manufacturing Cluster of Kanpur

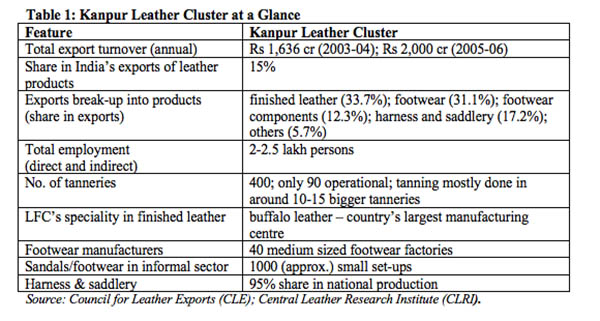

I. Introduction 1. Contrary to prevalent notions about such industries, the complex processes through which leather and footwear are produced require sophisticated knowledge and high levels of skills. 2. We identify three key aspects of traditional advantages of the LFC which have enabled it to adapt to changing contexts and demands and sustain itself over long time: flexibility, cooperation amongst the actors, and the skill levels of the workers. 3. We argue that, paradoxically, skilled labour and artisans, who are the core of the recent success of the cluster and the primary reason for its sustenance, are the ones who are being squeezed continually, almost to the point of extinction. 4. We argue that the pauperisation and immiserisation of labour cannot be understood till we place the cluster in the context of the entire global value chain into which it has been increasingly integrated, and appreciate its precarious position within that. 5. In the final section we provide an overview, and discuss the paradox of pre-capitalist relations of local production in the LFC being overlaid by the capitalist logic of globalisation. II. The Leather and Footwear Cluster of Kanpur1 The leather cluster of Kanpur dates back to the beginning of the nineteenth century, to serve the needs of the East India Company troops for leather and leather products. Its production grew with the Empire. By the end of the Second World War, the Kanpur-based Cooper Allen & Co. had emerged as the largest producer of army footwear in the world. After 1947 the demand for army boots declined, and with it the organised leather industry of the city. Besides army footwear, Kanpur was a large centre for manufacturing chappals (informal footwear) in the unorganised sector. The revival of the cluster took place in the 1970s, when leather started being exported from Kanpur in large quantities. At present this cluster produces leather and leather products like footwear, saddlery and harnesses and other miscellaneous products. Table 1 summarises some of the basic features of the cluster.

There is very little hard data available on employment in the cluster, and the figures are based on informed estimates.2 Further, given the peculiar nature of small industry clusters (as opposed to large organisations), the situation is very amorphous and dynamic. Employment fluctuates with number of orders, seasons, and other contingent factors. Even the larger organisations in the cluster depend significantly on a putting-out system for specific components. The increasing presence of seasonal migrant labour makes the picture even more complex. And yet, developments in the last two decades have affected the decentralised production practices in the cluster, and there has been a perceptible shift towards formation of larger organisations with most activities done within the factory premises. Production process in the leather industry Hides and skins

Offtake of hides

Hides market

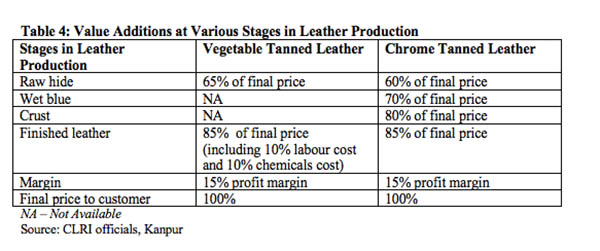

Selection of hides Tanning Traditionally the Kanpur Leather Cluster did only vegetable tanning, especially suitable for producing heavy buffalo leather in which this cluster specialised. Vegetable tanning needs wattle bark (the tannin agent) and a lot of water, and though it takes longer to tan leather through this process, it is relatively effluent free. Till the 1980s all leather tanned in Kanpur was vegetable tanned. Even today some tanneries specialise in vegetable tanning, but today in Kanpur leather is predominantly chrome tanned. Kanpur has 400 registered tanneries, of which about 90 produce vegetable tanned leather, around 60 both vegetable and chrome tanned, and the rest exclusively chrome tanned. However, production in most of the units is negligible, and gradually the smaller players are getting squeezed out of the market, as will be elaborated later. Leather from the tannery is sold out at several stages – wet blue, crust and then finished leather. Almost all the major environment pollutants are within the wet blue stage – the main pollutant being the basic chromic sulphate. But apparently this stage need not be as polluting as it is in this cluster, if only the tanners were to adopt more efficient chromium usage processes. Table 4 gives a rough estimate of the value additions that take place in the primary processing of leather – from raw hides to finished leather.

Footwear manufacturing Footwear manufacturing in factories

Methods of shoe construction III. The sustainability of the LFC of Kanpur The Kanpur LFC is more than two centuries old and has survived, grown and adapted itself to continuously changing conditions. The cluster has found fresh markets, got into new sets of products, and has adapted to changing production processes, government policies, and so on. According to our understanding, the Kanpur LFC has enjoyed three key aspects of traditional advantages, due to which it has been able to sustain itself over a long time and adapt to changing context and demands: the skill levels of the workers, flexibility, and cooperation amongst the producers (only the first one is discussed here, for the latter two see the longer version at 47/leather.html). Highly skilled workers in the LFC The following quote from a top-level executive in the leather industry captures the process of transition for certain specific castes in the cluster from selecting hides to becoming a tannery owner: All of them (the leather businessmen), well at least most of them, had come from Ballia, though I would not know for what historical reason but most likely as raw material (hide) suppliers – they were called ahratis. Even now there are individuals procuring leather from the village centre in and around Kanpur and getting them to the city bazaar – chamda mandi. As business improved some of them made the transition from hide procurer to distributor. As you would know in our society persons who handle hide with their own hands are the lowest in the social hierarchy and the transition would be motivated both by economic as well as social reasons. Gradually some of the individuals of this community moved into tanning of leather and often this social upgradation led them to discard their earlier business. Three broad categories of people went into tannery business – the Kasais, the Chikaras and the Bisatis. The Kasais are the ones who slaughter the animal – the Chikaras are probably the ones to skin the animal and also shave off the body hair from the carcass… These persons have a natural advantage because of their understanding of the quality of leather and their existing contacts in the rawhide mandi. The most crucial aspect of running a successful tannery is the choice of leather. It is very difficult to assess the quality of the hide under the grime and hair, and often sheer trust is the most important criterion for correct selection. Usually the source of the raw material gives an indication of the quality of leather – so you have to know ‘ahrat ka maal kahan se aata hai’. The Bisatis are the Muslim traders and the whole Parade and Meston Road are full of them and they got into the business primarily because of their association with the British. They would see the modernised tanneries and its economic possibilities and then some of them went in leather. IV. Degradation and pauperisation of skills in the Kanpur LFC Though the cluster has been able to sustain, grow and move in new directions primarily due to the high levels of skills of a large set of workers, paradoxically, it is precisely this resource which is being degraded and pauperised in the same period. In this section we will discuss different facets of this problem in different stages of production. Work conditions and labour in the tanneries 1. In peak periods the tanneries operate for 24 hours a day and workers work in two shifts of 10-12 hours each. Most of the tanneries of LFC are located in the Jajmau area, though some of the prominent ones have shifted to the other side of the river Ganges to the district Unnao. Most of the workers live in close proximity to the tanneries in the low land near the river. According to an informed estimate around 1.5 lakh workers and their families live in and around Jajmau. Among the workers living in Jajmau there were 60 percent Muslims and 40 percent Hindus. (An interesting feature of this cluster is the high degree of communal harmony that exists here. Kanpur, with a significant presence of both communities, otherwise has been afflicted with communal disturbances in recent years. The frequency of communal riots has increased with the decline of industries in the city and may be correlated with the rising unemployment in the region. And yet Jajmau has not witnessed any serious communal conflict in the last three decades.) 2. There are very few permanent workers in the tanneries (source: interviews with tannery workers in the LFC) and the permanent employees are largely those in staff positions. For example, in one of the largest set-ups, employing 1200 workers, there are only 298 permanent employees on the rolls, who include the accountants, security personnel, supervisors and marketing officials. The permanent workers are paid at around Rs. 110 per day. They get Sundays off with pay and also get a few days of paid leave annually. There are provisions for sick leave and other legal facilities such as Provident Fund, gratuity, etc. The temporary workers get Rs. 50 to Rs 70 per day with no allowances. 3.Another common practice to evade the provisions of labour laws is to record the employees as contract workers. Apparently labour laws are applicable to only organisations employing more than 20 workers. So the tannery owners divide their total workforce in groups of 19 and put a contractor at the head of each of these groups to supervise them. Thus the company may actually employ hundreds of workers but would not come under the jurisdiction of the labour laws. 4. Labour laws are regularly flouted in these premises – with the tacit support of the administration. There have been no effective unions in this industry to safeguard the interests of the workers. The working conditions inside the tanneries in LFC are extremely hazardous and almost no safety measures are taken by the employers – not even basic working gear like gloves and boots are provided (source: interview with a union leader of a small union in Jajmau, Kanpur LFC, unaffiliated to any party). In most tanneries in Kanpur the workers are required to handle toxic chemicals at various stages of the tanning, including the tannin agents, colouring agents, acids, etc. Both physical handling and inhalation have serious repercussions on the worker’s health (source: interview with a tannery worker in Kanpur LFC). The press regularly reports serious and even fatal accidents in the Kanpur tanneries. Even in the best of the facilities the conditions are very unsafe, as we found out during our field visits. The description below is from our field notes during a visit to one of the bigger tanneries in Unnao:

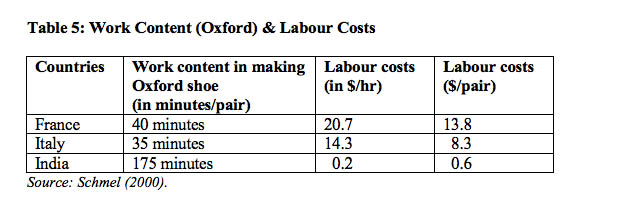

5. Attempts to unionise the thousands of tannery workers have been largely unsuccessful. This is because of precipitous rise in unemployment in the city due to the decline of the textile industry. The leather industry, as the only thriving employment option of any significant scale in the vicinity, has had to absorb the pressure of this loss. The situation has got further aggravated in recent years because of the large influx of workers from neighbouring states of Bihar and Chattisgarh. These workers have brought down the existing wage rates significantly. According to an informed estimate the immigrant workers constitute about 25 percent of the working population in the cluster. Conditions of work and terms of labour in the footwear factories And yet, increasingly, footwear production is shifting to Third World countries. This can be explained by the extremely low wage rates existing in these countries as shown in Table 5. While France has operator-hour working costs of $20.70 and Italy $14.30, operator-hour working costs in developing countries are $0.20- 0.50. Thus for a similar shoe the labour costs in France are $14, in Italy $8 and in India only half a dollar. Not only are the wages paid in the developing countries very low, at below $1.60 for a 10 hour working day (with barely an hour of break), there is almost no social security provided by the State to the workers and their families. The extremely low labour costs obviously lead to inefficient use of labour in production processes in the developing countries.

As an illustration, the account below describes the wages paid to a worker we interviewed during our study, who has been working for a fast growing exporting unit for the last 13 years.

Working conditions and labour in factories 2. From several accounts it seems that the work in the factory has become tougher since the introduction of the mechanised production process – especially the conveyer belt. Though the level of production and the general uniformity in quality has increased, there has been a decline in individual or even collective discretion in the production process. Thus the pace of production does not leave any slack for breaks from this monotonous work. In some factories during busy season it is reported that the factory owners lock the workers inside during the night. That is apparently so that the costly machinery, unfinished and finished goods and material kept in the factory are not stolen. 3. As described earlier for tannery workers there are no industry-wide unions in the organised footwear sector either. Attempts at unionisation within a factory, though rare, have taken place in the recent past. But they have been largely unsuccessful and the owners have come down heavily on the workers who were identified as leading the effort. The following incident, which occurred in an upcoming footwear factory, describes the pattern in most of such efforts.

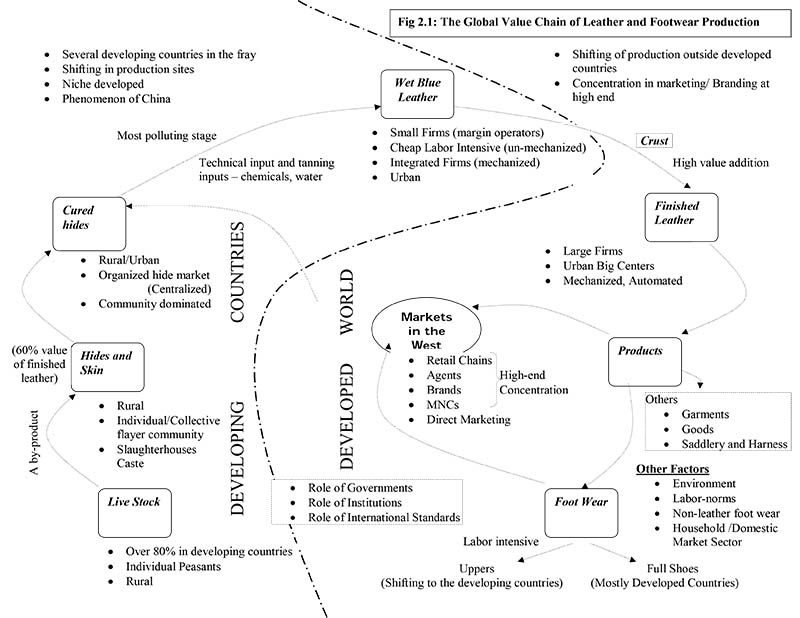

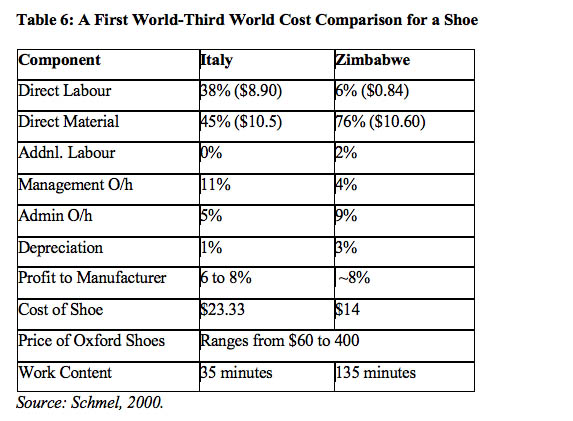

V. Situating the Kanpur LFC in the global value chain World leather and footwear market Of the ten countries that were identified as the leading producers of footwear in 1998, China accounts for almost 50 per cent of the world production. India with an annual production of 680 million pairs of shoes came second to China, though it accounts for merely one-tenth of the Chinese production. In Central and South America, Brazil and Mexico are large producers for the region and are among the top ten world producers. Italy was the fourth largest producer in 1998 and the main European producer. India did not feature in the top 10 footwear exporters of the world. A defining feature of the global footwear trade is that while most of the footwear were produced in the developing countries, the bulk of it was consumed by the Western countries (SATRA, 2003). Of the total 3390 million pairs traded in 1998, 3130 million pairs were exported from Asia. Around 51 percent of the total world footwear exports was headed for the USA, while around third was consumed in Europe. According to survey done by SATRA (2003) the top per capita consumer of footwear in the world was the US, with an annual per capita consumption of 6.2 pairs of footwear, followed by European countries with over 5 pairs of footwear consumed annually. Thus the world trade in footwear is divided between countries which produce footwear (mostly developing countries in Asia) and the ones where they are consumed – the industrialised countries of Europe and America. Exports of Indian leather and leather products The Kanpur LFC in the export market 1. Several industry insiders suggest that in Kanpur, and actually in India as a whole, there are no unique skills or technology which can ensure a secure niche in the international market, and the whole market is hinged on cheap prices. And therefore the market can shift out to some other Third World countries – such as Peru, Brazil or, more likely, China, which may offer even lower prices. This is amply borne out if we analyse the break-up of the monetary value chain of these products. Table 6 provides a First World-Third World comparison between Italy and Zimbabwe for the making of an Oxford shoe. The figures for Zimbabwe would be very close to those existing in the Kanpur LFC. As is evident, while in the Third World clusters, the labour component is barely 6 per cent of the finished shoe and barely 1 per cent of the lowest retail price of an Oxford shoe ($60), labour costs in Italy is close to 40 per cent of the finished shoe. The direct material constitutes over three-fourths of the total cost of production of a shoe in the Third World, and since many of the components constituting this head (except for finished leather) come from the First World countries, their prices remain largely non-negotiable. Hence the only factor which can be (and is) squeezed any further, in spite of being at the border of subsistence, is labour wages. Thus the arithmetic of the global value chain is detrimental to labour both in the First World as well as the Third World. Jobs get pushed out of the First World because of the abominably low wages in the Third World, rendering workers unemployed in the developed countries. And since price is their only competitive advantage, the Third World clusters are forced to depress wages even further to remain in the market. Given that the more machine-intensive components are sourced from the developed countries, the First World also corners a large proportion of the cost of production of the shoe besides getting it cheaper.

Secondly, as is evident from Table 6, a considerable part of the final value to the consumer is accounted for by the marketing part of the chain. This is true for both the First and the Third World clusters. Almost 80 per cent of the final price of the shoe goes to the long chain of middlemen who operate only in the post-production stage. Or in other words, four-fifths of the ‘value addition’ of shoes in the global value chain actually adds no value to the product. 2. The structural asymmetry of the value chain between the production part situated within the clusters and the marketing part outside as part of the global chain is also evident in our interviews. Repeatedly the respondents spoke about the disadvantageous position that they found themselves in during marketing and its deleterious consequences for their individual units and processes within the cluster at large. An important drawback of such a long chain is the inability to check the credibility of a geographically distant client, which might lead to serious losses in case of default of payment. There is fierce in-fighting among organised footwear manufacturers within the cluster for international orders. All kinds of ethical and unethical practices are employed to secure foreign customers. Prices are under-quoted, designs stolen, customers intercepted, skilled workers poached, agents bribed and customers stolen – all these of course are described as shrewd marketing techniques. The foreign customer is the ultimate gainer in the intra-cluster infighting for price and orders. They are treated lavishly by the producers during their visits. A factory official described a typical visit:

Though some kind of cluster-wide associations may help in striking a more reasonable bargain, such institutions are absent and are unlikely to emerge given the present context. An industry expert describes the vulnerability of most producers in the cluster in the following account.

With the rise of large chains like Wal-Mart as the global buyers this relationship has worsened further. An erstwhile executive director of Council for Leather Exports (CLE) narrated how the industry chartered a whole aircraft for the regional executives of Wal-Mart to showcase Indian leather products to them. The constant threat of losing the market to other Third World clusters or to a competitive producer in the same cluster makes them quite subservient in their negotiations with the Western buyers. 3. The Kanpur Leather Cluster caters primarily to the international markets, but the footwear headed out from the cluster caters to the lowest end in the Western market. The niche for the Indian footwear producers in the international market is mostly the prices, and since this is true for almost all the Third World producers there is fierce bargaining for every cent. The Government of India provides an incentive of a percentage of the value of exports to promote exporters. Many exporters survive the initial years and lean periods on this incentive. This is a fixed amount and depends on the amount of value addition done by the manufacturer. For example, the incentive is 9.6 per cent for shoes and 6 per cent for sandals on the FOB prices of the consignment. This is worked out by the CLE based on a country-wide survey on the costing involved and the margins available for various types of products. VI. Paradoxes underlying the global positioning of the Kanpur LFC As we have repeatedly emphasised, the primary strength of LFC is the continuous supply of skilled labour required to handle various steps in the manufacturing of footwear and leather, that too by the means of a natural ‘raw material’ such as an animal hide. We have also tried to bring out the complexities involved in production of leather and manufacturing of footwear, to dispel the popular notion that ‘traditional’ industry requires little skills. We would like to assert that merely because some skill is in large supply and a set of people have developed means and ways to master it without any apparent resource investment, it cannot be construed that the work involves ‘low skills’. And further, low wages do not always mean low skills; the reverse, i.e., that high wages imply high skills, is even less true. A good example of the latter is the business process outsourcing (BPO) industry. But while skilled labour is the primary strength of the industry, it is precisely this component which is persistently being squeezed, and in the process, degraded in the LFC. While labour costs are less than 10 per cent of the total manufacturing cost of footwear, the labour costs are mere 2 per cent of the price at which the same shoe is sold in the international market. And yet industry circles, policy pronouncements and popular media persistently proclaim that the clusters ought to increase their ‘competitiveness’ and improve ‘export performance’ through ‘efficient’ usage of labour. It defies understanding as to what can be achieved by squeezing the 2 per cent part of the chain, especially if this is the very foundation of the whole structure. Other parts of the chain, especially the long margins of up to 75 per cent in the global marketing through various intermediaries and international brands, are taken as given, as aspects about which ‘nothing can be done’. Even the periodic attempts at ‘cluster development’ by the Government and other State and international agencies, are primarily for finding technological solutions without any appreciation of the basic problem. This approach essentially boils down to automation and replacement of workers by machinery. ‘Solutions’ like CAD-CAM (computer-aided design and computer-aided manufacturing) are bandied about repeatedly as the answer to the ills and problems of the LFC. In a place where even basic infrastructure such as electricity is not available (long power cuts in the industrial areas of Kanpur are routine), how can CAD-CAM even be implemented? Another significant fall-out of the availability of cheap skilled labour is that it is used in a wasteful manner, leaving little scope for mechanisation and technological upgradation. Thus in spite of the Kanpur LFC and the other leather clusters making the Indian leather industry a significant global exporter, almost all the machinery employed here is imported. The labour in the Kanpur LFC is caught not only in capitalist relations of ‘demand and supply’, but is also bound by all kinds of caste-based ties due to the ‘lowly’ status of work involving leather. For instance, there are sharp divisions in terms of sub-castes which can handle various parts of a dead animal. Some of the castes which we could identify were the Raidas, Kol, Khatik, Dhanuk, Passi, and Balmik, and (among the Muslims) Kasai, Chikara, and Bisati. They handle various parts of the dead animal – the hair, the bones, the tallow, and also the various processes in its primary preservation. It is similarly worth noting that in case of fallen carcasses, the main reason for non-recovery is the social stigma attached to the activity. At present the whole activity is carried out with inhuman techniques and under very unhygienic conditions. The Kanpur LFC is increasingly getting integrated in a global manufacturing and distribution chain as a subordinate actor to the global interests, a situation not very different from the colonial times. Paradoxically, as the actors of the LFC are getting increasingly integrated in the global chain they are getting completely disconnected from the domestic market, and even from one another within the cluster. In Section V we have discussed at some length how exporters have to compete against one another in the cluster to maintain a toehold in the global market. There is also an increasing disengagement between the smaller players and the larger ones. During our field work we found that gradually small units, both among tanneries and in footwear manufacturing, have got almost completely cut off from the big exporters. These large players have built up integrated units and have become self-sufficient, and when required prefer to source their needs from fellow exporters rather than the smaller units. Though there are around 400 tanneries in the Jajmau-Unnao belt as mentioned earlier, the number actually working are much lower. Actually, given the large export component in the Kanpur Leather Cluster, only the larger players are able to survive the uncertainties of foreign orders. Further, unlike in the 1980s, at present the export of finished leather has declined significantly, and there is a growth in the export of leather products; since only big organisations are in that business they prefer to have integrated units where they perform the entire process from the raw hide stage to the finished good. Of late several tanning units have gone into job-work in a big way. The worst hit are the smaller tanneries, which do not have adequate buffer to absorb reverses in business, and they are by and large getting squeezed out. An even more alarming trend is the complete dissociation with the domestic market. Thus though Kanpur cluster has grown rapidly in recent years, it has virtually no presence in the domestic market, especially in the case of the bigger exporting units, barring one notable exception (which is not into exports). None of the players has any serious plans to enter the domestic market. This obviously is a short term policy, given that the export market is extremely competitive and keeps fluctuating, as is evident from the present global slump. The industry, in response, is clamouring for all kinds of incentives from the Government. In one more significant way the LFC has become integrated in global geo-politics, by becoming a means for passing off the environmental costs of the First World to the Third World. Leather tanning is anyway water intensive, and in the Kanpur LFC it is even more so because of extremely inefficient usage. Thus another factor which makes it possible to produce cheap leather and shoe in Kanpur is the abundant supply and massive usage of water for which the producers do not have to pay. At present there is no crisis of water supply for the LFC operators because of the LFC’s location in Indo-Gangetic plains. And yet the fertile agricultural land surrounding the cluster is already experiencing a steep decline in underground water table levels. Similarly, little investment has been made to actually control water pollution caused by the running off of highly poisonous metal effluents and wastes into the nearby Ganges, other water sources, ground water and village fields. Thus, in the final analysis, the villagers and other users of the water are subsidising the First World consumers of the products of the LFC. This has been a global trend, and is the reason for shifting of the most polluting stages of leather tanning, especially till the wet blue stage as depicted in Figure 1. Finally, the State has been conspicuous by its absence, especially in formulating any long term policy framework for a sustained development of the cluster. All that the Government has provided is short term incentives and subsidies so that the cluster can quickly hop onto the export bandwagon without any preparations or buffer to handle eventualities like the present global recession. In the name of cluster development the State has only been providing support for fancy technological upgradations like computers and the like. There is neither the will, nor any mechanism, to understand the basic problems, with the aim of evolving a long term programme to address them. According to us, probably the most basic problem is the lack of any labour standards and absence of regulatory bodies to enforce them. By labour standards we mean minimum conditions for a worker relating to wages, hours of work, employment of children, safety, working conditions, etc. Till some minimum systems are put in place to regulate the conditions at work and wages of the workers in the cluster, no significant and long-term improvement can take place in the cluster, and the State has to play a role in this. Even the experiences of the famed clusters in the Third Italy suggest that neither improvements in product quality nor production processes took place there till there was a guarantee of minimum labour standards. But given the present blinkered policy framework this is not even in the realm of debate by the Indian State or other agencies. The present account is not meant to be a “chronicle of a death (of the LFC) foretold’. On the contrary the exercise has been done as we foresee significant possibilities of growth and organic development in the cluster. Large industry-led growth in Kanpur during the colonial period (like in textiles) did not result in sustainable development, while the small industry leather cluster has survived, adapted and grown in spite of negligible outside intervention. Further, as has been argued all along, this has been possible because of the availability of skilled workmen and other important resources like the basic raw materials (leather, water), entrepreneurial skills, cooperation amongst the actors, etc. And yet, in spite of all these innate advantages, the cluster’s future seems to be in jeopardy simply because of the uncertainty of demand, which is often manipulated by the long chain of intermediaries operating between the producers and the consumers. At present the cluster is dealing with this serious threat by cheapening their products, mainly through pushing down the wages even further. Unfortunately this tactic is not only threatening the very existence of the skilled workforce, but is also one which is being employed by almost all the Third World clusters. With an average of 5-6 pairs of footwear bought by Europe and USA annually, the total international demand is unlikely to increase dramatically in future, and is practically saturated. Thus the Kanpur LFC, given the present dispensation, would continue to witness unhealthy competition from both within and without; and the individual maximising strategy adopted by its players would ruin the basic advantages, leading to an inevitable decline of the cluster. We feel that this negative spiral can be effectively reversed into a positive loop by fostering a sizeable domestic demand. Demand from the domestic market is likely to be less uncertain compared to the international market. Further, it would have the added advantage of being unencumbered by the long chain of intermediaries, resulting in bigger earnings being retained within the cluster. And, lastly, we think effective demand can be created only by a sincere appreciation of the fact that the large workforce in the cluster are not merely a factor of production, to be bought at the lowest possible price, but actually are the main producers and potential consumers too. Hence giving due wages and relevant benefits to the workers, while increasing the production costs marginally, would be essentially an investment if seen in a broader macroeconomic perspective, as it would create an effective demand for footwear (and other products). After all, every pair of skilled hands, needs a pair of footwear too, only they often cannot afford it. Or in other words, we think that a vibrant domestic demand would effectively draw out the LFC from the uncertainties of the global value chain and provide the necessary buffer for a sustainable long term growth. Of course, the creation of such demand requires broader changes beyond the scope of our article. References 1. All India Survey on Raw Hides and Skins (2005), CLRI, Chennai. 2. Cameron Kippen (2004): The History of Shoes: Shoe Making, Department of Podiatry, Curtin University. 3. Council for Leather Exports (CLE), Facts and Figures and Statistical Data, 2006. 4. Schmel, F. (2000), Structure of Production Costs in Footwear Manufacture, UNIDO. 5. The Leather Global Value Chain and the World Leather Footwear Market, (2003). A sponsored article by World Footwear and Leather Manufacturers, SATRA. 6. International Council of Tanners, 2000 7. World Foot Wear, Vol. 13, No. 3, 1999 8. World Statistics, ITC, Geneva. 9. India’s Exports, Director General of Commerical Intelligence & Statistics (DGCI & S). 10. World Leather Market (2000) Investor Services & iNES, © Fact book. 11. H. Schmitz (2000) IDS Working Paper 100

Notes: 1. The primary data is based on field visits, interviews and observations conducted during 2004-2006 with various constitutencies in the cluster – manufacturing units of various kinds, markets, important individuals, like association heads and union functionaries, markets, research and financial institutions, independent professionals, etc. (back) 2. The total employment figure in Table 1 is an aggregate of the flayers, workers in the tannery sector, harness and saddlery business, footwear sector and the unorganised chappal sector. (back)

NEXT: Kanpur Leather Cluster Revisited |

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2018 by Research Unit for Political Economy |

|