No. 61, June 2015

| |

|

|

No. 61, June 2015 |

|

|

Nos. 61 Making Room in India – for Whom? Bank Board Bureau: Another Step toward Privatisation and Foreign Takeover Public sector banks: Reform by Death

|

Public sector banks: Reform by Death The Government is determined to put several public sector banks to death. This is not an accusation leveled by a trade union leaflet or a political opponent of the Government. Rather, this plan has been spelled out and recommended, in precisely these words, by the current Chief Economic Adviser (CEA) to the Government, shortly before he assumed that post. The Government is busy implementing that plan, as we can see in the present Budget. The objective is the private take-over of India’s banking sector. Discussion on the staggering consequences of this plan is virtually absent from corporate media outlets (some of which, indeed, are themselves deeply involved in the private financial sector). Before describing the CEA’s plan, let us explain the background: Paucity of funds as an alibi for privatisation The finance minister, in his 2014-15 Budget speech, estimated the sum required by 2018 at Rs 2,40,000 crore (Rs 2.4 trillion). This means that the Government would have to pump in additional budgetary funds if it wished to maintain its stake at its present percentage (its stake in different public sector banks ranges from 65 to 80 per cent today).

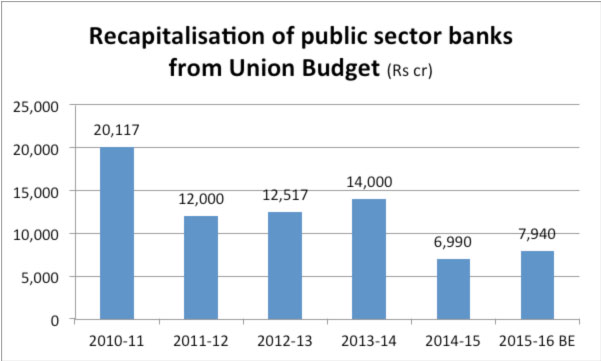

(ii) The Government did pump some capital into the banks till 2013-14, Rs 58,600 crore between 2011 and 2014, including Rs 14,000 crore in 2013-14 alone – no doubt, far short of Basel III requirements. Nevertheless, in its 2014-15 Budget, the Modi government reduced the allocation to Rs 11,200 crore; it proceeded to slash this drastically in the course of the year, so that only Rs 6,990 crore was actually given. Another, radical, plan was in fact afoot. The plan was to privatise the banks, in the name of strengthening them. (iii) In May 2014, the RBI-appointed Nayak committee on bank governance (about which, more later) called for reducing the Government stake in public sector banks. In December 2014, the Union Cabinet issued a communique stating that “Capital requirements of banks have increased under Basel-III. The quantum of capital support needed by banks is huge, which cannot be funded by budgetary support alone. If the public sector banks are permitted to bring down Government holding to 52 percent in a phased manner, they can raise up to Rs.1,60,825 crore from the market.” Paucity of funds, and the binding constraint of fiscal deficit control, were made into an alibi for phased privatisation of public sector banks. Selective recapitalisation The 2015-16 Budget continues this practice, reducing the budget for recapitalisation to Rs 7,940 crore, a 29 per cent cut from last year’s budgeted figure. The Government will continue with its policy of selective recapitalisation. Even if one were to accept the strange notion that the Government should ration out funds only to a chosen few banks, the criterion used was even stranger. Note that the Government did not set a particular standard of performance as the cut-off. Rather, it simply excluded all those ‘worse than average’. Since roughly half the banks inevitably would fare worse than average, this method was entirely intended to set half the public sector banks adrift. It is estimated that these excluded banks would need roughly half the additional capital required for all the public sector banks. The earlier Government stance – of backing the public sector banks as a whole – anchored their financial stability, enabling them to extend credit for economic activity even during an economic downturn. In line with this implicit Government backing, the credit rating of all the public sector banks at that time was very nearly the same. Now, by contrast, promptly after the Government did its selective recapitalisation, Moody’s announced that it was downgrading the credit rating of two public sector banks, Central Bank of India and Indian Overseas Bank to “below investment grade”. This would make it harder for them to raise funds from the market too. With neither Government nor market as a source of capital, these banks have little option but to merge with stronger banks. The Indian arms of international credit ratings agencies noted that the Government’s move set the stage for a “shake-up” and “consolidation” – i.e., the takeover of financially weaker banks by stronger ones, either in the public sector or even the private sector. Starving the banks and selectively recapitalising them is thus a strategy to eliminate some of them. The Economic Survey 2015-16 says

Where did the NPAs come from? The second type of NPA is in consumer loans for the purchase of flats and cars, which ballooned during the boom and in some cases turned sour with the downturn. The UPA Government tried hard to revive the growth of the economy through expanding such loans. The then finance minister Chidambaram went so far as to tie capital infusions to public sector banks to their expansion of consumer loans (e.g., lend Rs 60,000 crore for the purchase of flats and cars, and the Government gives you Rs 6,000 crore as fresh capital). Even more intense was Government pressure on public sector banks to lend to the third category of NPAs, the corporate sector. These were concentrated in sectors such as ‘infrastructure’. To a large extent, the economy’s growth model was based on such ‘private’ investment using public funds. The best-known case was of Kingfisher Airlines, which excelled in flying capital out of the country. The entire boom of 2003-11 would have been impossible without the public sector banks footing the bill for private investment. Outstanding bank credit to infrastructure grew more than 100 times during the boom (from Rs 724 crore in 1999-2000 to Rs 78,605 crore in 2012-13, a compounded annual growth rate of 43.4 per cent over 13 years). A deputy governor of the RBI pointed out:

Elsewhere, he also pointed out that it was corporate borrowers who accounted for the bulk of bad debt; bad debt made up a bigger share of their total borrowings than in the case of small borrowers, but they have been treated leniently by the banks, which ‘re-structure’ corporate debt in various ways (re-schedule payments, reduce interest rates, swap debt for equity, forgive debt, index interest payments to earnings, etc.) – leniency they do not show to small borrowers:

Thus NPAs caused substantially by the private corporate sector are now being advanced as a reason for the Government to privatise the public sector banks (albeit in a somewhat disguised manner). Reform by death Subramanian said that the award of new banking licenses for private sector banks would not suffice: “the share of public sector banks in total banking (measured as a share of assets or deposits) has stubbornly persisted around 75 per cent…. So, going forward the fact of more private banks is no guarantee of reducing the role of public sector banks.” He proceeded to spell out an “indirect way of privatising them”:

Subramanian’s column was appropriately titled: “Indian banking – reform by death”. Its recommendations evidently did not come from the top of his head; rather, they reflected well-laid plans among the top circles in foreign finance, the RBI and the government. Action along these lines swiftly ensued. Subramanian recommendation: “As growth declines and exposes the fragility of some of the public banks in the form of rising non-performing loans, the RBI should be brutal in its assessment of them, erring on the side of declaring some banks as unviable commercial institutions.” Action: In May 2014, the RBI-appointed Nayak committee, to which we referred earlier, began its report by declaring ominously: “The financial position of public sector banks is fragile, partly masked by regulatory forbearance”. That is, only the RBI’s leniency allowed them to survive. Such a statement appears calculated to spread fear and panic among the public about these banks. Whereas in fact, as long as the earlier Government backing for the public sector banks continued, such fears were baseless. It was, then, only the Government itself that could generate such fear, by making it clear that it would no longer support them. Subramanian recommendation: Public sector banks in trouble should not be given fresh capital infusions; rather the crisis should be used to shrink the public sector, and transfer its “good parts to the private sector”. Action: The Modi government not only starved the banks of capital, but has recapitalised selectively, not only shrinking the market share of half the public sector banks, but sending a signal that they are on their way out, to be taken over by others. Criticism of State policy is frequently labeled ‘conspiracy theory’, a magic phrase which, once pronounced, renders it unnecessary to refute the criticism itself. But in this case, those in power have themselves spelled out the conspiracy quite explicitly; no theory need be put forward by their critics.

NEXT: Back to Table of Contents

Notes: 1. K. C. Chakrabarty, “Infrastructure Financing by Banks in India: Myths and Realities”, RBI Bulletin, September 2013. (back) 2 .K. C. Chakrabarty, “ Two Decades of Credit Management in Indian Banks: Looking Back and Moving Ahead”, RBI Bulletin, December 2013. (back) 3. Arvind Subramanian, “Indian banking – reform by death”, Business Standard, 7/3/14. http://www.business-standard.com/article/opinion/arvind-subramanian-indian-banking-reform-by-death-114030701184_1.html (back)

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2015 by Research Unit for Political Economy |

|